Summary:

- Proof-of-stake networks securing tens of billions in assets rely on stakers and validators whose distinct economic roles are poorly served by current U.S. tax rules—creating compliance burdens and competitive disadvantages for domestic operators.

- Two unresolved tax issues—the timing of taxation on staking rewards and the sourcing of staking income to validator location—are actively pushing infrastructure, investment, and technical talent offshore, as documented by CCI member reports.

- Congress should clarify that staking rewards are taxed at sale (not creation), that sourcing does not depend on validator location, and that staking income qualifies for existing carveouts available to tax-exempt investors and digital asset investment structures.

- For more articles like this, please visit our Explainers page.

Download CCI’s handout on staking issues.

Staking as Critical Infrastructure

Proof-of-Stake (PoS) is an increasingly popular form of blockchain validation due to its efficiency and security. PoS blockchain networks have become critical infrastructure for the digital asset ecosystem. Ethereum holds over $68 billion in total value locked. Solana processes a high volume of both financial and non-financial transactions. Avalanche is increasingly serving as an institutional bridge into crypto. These networks—and the validators and stakers who secure them—depend on clear, workable tax rules to function effectively in the United States. Right now, those rules don’t exist.

What Is Staking?

In proof-of-stake networks, decentralized validators verify transactions and add blocks to the immutable ledger. To participate, validators must lock up crypto assets as collateral (their “stake”) to earn newly created tokens as rewards for committing resources to support honest validation.

Participants can engage via two methods:

- Operate their own validator nodes and engage in “solo staking” (this requires technical expertise and meeting protocol-specific requirements, making it rare – fewer than 6% of all validators)

- Delegate assets to staking-as-a-service providers who handle technical operations for a fee. Providers can serve both institutional clients and retail investors.

Enhanced Stability and Security

Protocols require staked assets to remain locked for periods ranging from minutes to weeks after which users can freely transfer or sell their tokens. These lock-up requirements discourage short-term speculation and promote network stability. Honest validators are rewarded with additional tokens, creating positive economic incentives that make compliance more profitable than malfeasance.

The enhanced security staking offers comes from the fact that a successful attack on a proof-of-stake network requires controlling a majority of staked tokens (51%). Even if a malignant actor could afford this, the attack would crash the token’s value, destroying the attacker’s investment.

Key Actors in Staking

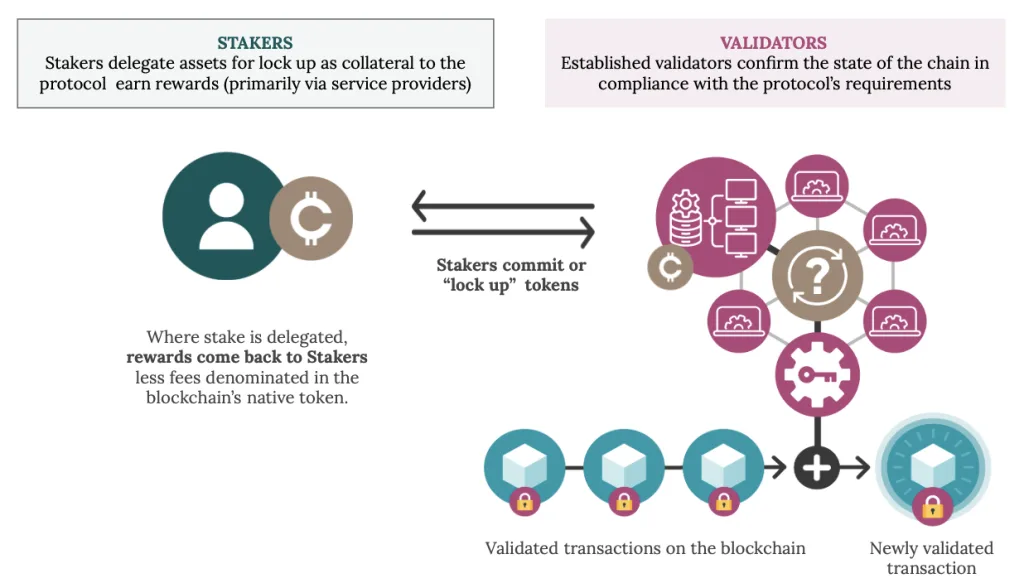

Understanding the tax implications of staking requires distinguishing between the two key actors in the process: stakers and validators. These actors perform separate functions in the staking process that should be considered separately from a tax lens.

Stakers provide tokens to be locked as collateral. The vast majority—around 94% of institutions and retail participants—use staking-as-a-service providers rather than operating their own infrastructure. After the lock-up period ends, stakers receive rewards from the blockchain in the form of native tokens. Critically, the value of those rewards is not realized until the tokens are sold.

Validators operate the physical infrastructure—servers, software, and the technical resources needed to execute validation. They may run a single node or many nodes, and they often hold tokens on behalf of multiple stakers. Validators are compensated through service fees and newly minted tokens, not from stakers’ principal. These are fundamentally different functions, and they warrant different treatment under the tax code.

The Core Tax Problems: Timing and Sourcing

Uncertainty around two specific tax issues is discouraging investment in U.S.-based staking infrastructure and pushing validators offshore.

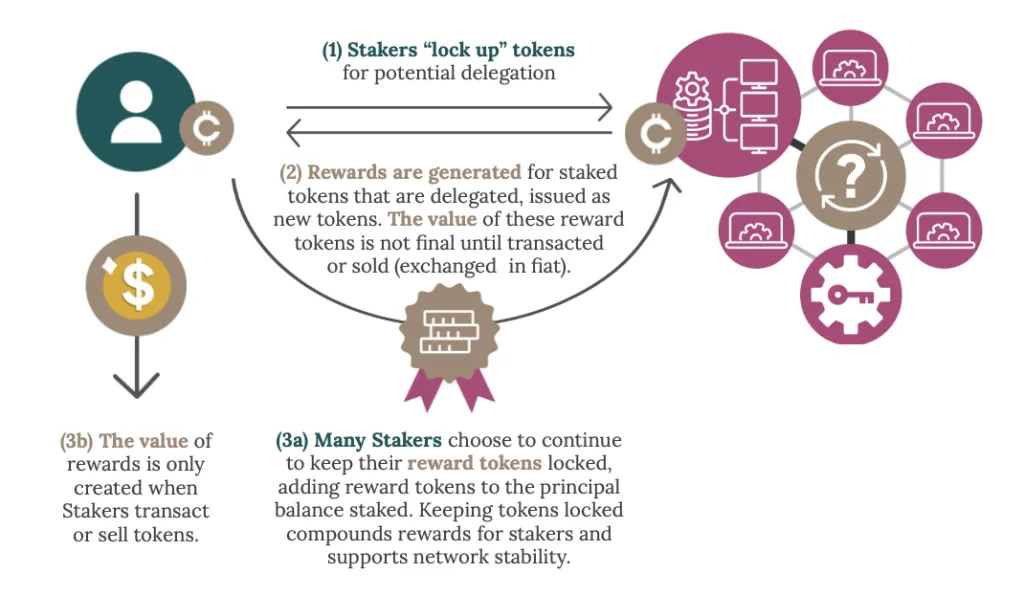

Timing. While staking generates token rewards, those rewards function as compensation for providing critical network infrastructure—not as immediately realized income. The value of reward tokens is not fixed at creation; it fluctuates with market conditions and is not economically realized until the tokens are transacted or sold. Many stakers choose to keep their rewards locked, compounding their principal and further supporting network stability. Taxing rewards at the moment of creation—rather than at the point of sale—misaligns tax liability with economic reality and creates a disincentive to continue staking.

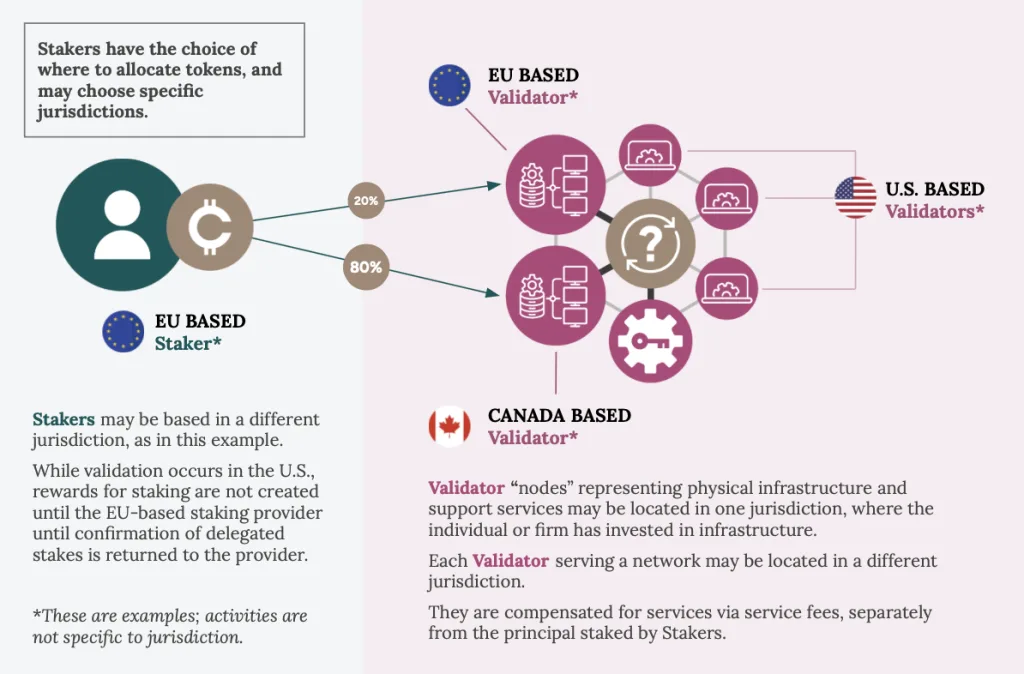

Sourcing. Because blockchains are decentralized, validator infrastructure may be located anywhere in the world. Under current guidance, tax advisors treat staking income as sourced to wherever the validator infrastructure is physically located—similar to how cloud computing income is sourced. The consequence: foreign investors who stake through U.S. service providers may face a 30% withholding tax simply because a validator node is based in the United States. This creates a direct competitive disadvantage for U.S.-based staking infrastructure.

The real-world impact is documented through market activity. In many instances, institutional clients—asset managers, custodians, exchanges, and venture firms—are contractually requiring that validators be hosted outside the United States to reduce UBTI and ECI risk. As a result, a majority of validators for many industry leaders are now located abroad, with a growing share in the EU and Canada. Infrastructure investment and technical talent that could be deployed domestically are going offshore instead.

“Many of our customers, both US and non-US, from all different business lines (asset managers, custodians, exchanges, VCs, etc) request we represent contractually that our validators are not hosted in the U.S. The requests are made to help mitigate any UBTI or ECI risk until clarity is provided. These are typically hosted in the EU or Canada as opposed to the US.”

— A major institutional staking-as-a-service provider serving U.S.-based clients

What Congress Should Do

Addressing these issues does not require novel tax policy—it requires applying longstanding principles to a new technology. CCI recommends that Congress clarify the following:

Tax treatment of staking and mining rewards. Staking and mining rewards should be treated like all other created property: taxed at the time of sale, not at the time of creation. This approach is consistent with economic substance and with how the tax code treats other forms of newly created property.

Source rules. The source of staking rewards should not be determined by the location of the validator. Decoupling sourcing from validator location would place U.S. staking nodes and service providers on a level playing field with foreign counterparts, removing the current incentive to move infrastructure offshore.

Unrelated Business Taxable Income. The investment income carveout from UBTI should be expanded to include periodic income from digital assets, including staking rewards. This would align the treatment of staking income with similar income for tax-exempt investors.

U.S. digital asset investment structures. While the IRS’s Revenue Procedure 2025-31 creates a safe harbor for staking in exchange-traded products, legislative action is still needed. Specifically, Congress should update the grantor trust rules to expressly permit staking activities within grantor trust structures, and update the “qualifying income” exception to the publicly traded partnership rules to include staking income.

The Bottom Line

Clear staking tax policy is not just good for the crypto industry—it is a prerequisite for keeping critical blockchain infrastructure and investment onshore. The current uncertainty is not a neutral state; it is actively shifting validator infrastructure, talent, and capital to other jurisdictions. Congress has the tools to fix this, and 2026 presents a clear opportunity to act.

CCI is conducting ongoing research on these topics and can share findings with congressional staff upon request. For more information, contact [email protected] or [email protected].