Summary:

- The Organization for Economic Development (OECD) recently published a new tax transparency framework known as the Crypto-Asset Reporting Framework (“CARF”).

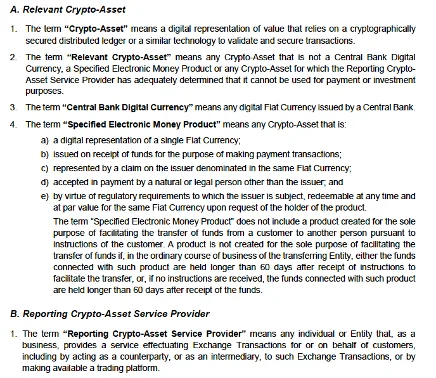

- The scope of the framework includes all “Relevant Crypto-Assets,” which includes NFTs but excludes three categories including Central Bank Digital Currencies (CBDCs), Specified Electronic Money Products and crypto-assets that cannot be used for payment or investment purposes.

- CARF may impact DeFi since obligations are placed on individuals or entities that exercise control or have sufficient influence over a trading platform.

- Read more Crypto Council policy briefs.

What is the purpose of CARF?

The OECD is an international organization of 37 countries working to address challenges such as economic development, education, and environmental sustainability. The US has been a member of the organization for over half a century.

While the OECD is not a law-making body, the organization encourages member countries to develop similar international standards, so that everyone plays by the same rules and cooperates to reach objectives that oftentime require cross-border participation.

For example, one of the key goals of the OECD is to promote tax transparency for financial accounts held abroad. In an effort to tackle this challenge, the OECD instituted the Common Reporting Standard (CRS) in 2014, which calls on countries to obtain information from their respective financial institutions and automatically exchange that information with other jurisdictions annually. Since the OECD adopted the OCS, over 100 jurisdictions have implemented the CRS.

While the CRS may have been instrumental for countries to gather tax information, crypto-assets present a unique challenge. Individuals can trade crypto-assets without using traditional financial intermediaries or a central administrator with visibility on these transactions. In simplest terms, the OECD is concerned that individuals trading crypto-assets fall outside of the CRS reporting regime.

To mitigate this concern, the OECD developed a new crypto-asset reporting framework (“CARF”), which aims to exchange tax information in Crypto-Assets automatically. In March 2022, the OECD released a public consultation document, seeking feedback from the industry on this framework. These consultation or feedback processes are fundamental to rulemaking and an important part of engaging directly with the industry. The Crypto Council responded with this comment letter.

What’s covered by CARF?

CARF places reporting requirements on intermediaries and other service providers such as crypto exchanges, crypto brokers and dealers, and crypto ATMs that facilitate exchanges of Relevant Crypto Assets. CARF defines “Crypto Assets” as digital representations of value that rely on a cryptographically secured distributed ledger or a similar technology to validate and secure transactions.

However, not all Crypto Assets are necessarily Relevant Crypto Assets that place reporting requirements on service providers. Relevant Crypto Assets exclude (1) crypto-assets that cannot be used for payment or investment purposes, (2) Central Bank Digital Currencies (CBDCs), and (3) Specified Electronic Money Products, which represent a single fiat currency and are redeemable at any time in the same fiat currency at par value.

What does this mean for NFTs?

Notably, this definition of Relevant Crypto Assets captures NFTs “traded on a marketplace,” which could create confusion or obstacles to responsible crypto use and effective reporting. For example, consider a gaming company that issues character skins as an NFT and explicitly states it is a collectible for the month’s top players.

CARF guidelines state that even if an NFT is marketed as a collectible, Reporting Crypto Asset Service Providers must make case-by-case assessments of the NFT’s use. If individuals can use the NFT for investment purposes, it is a Relevant Crypto Asset. However, this approach could lead to uncertainty and prohibitive reporting costs for companies intending to issue NFTs as non-investment items, especially as the use, technology, and legal status of NFTs evolve.

Individuals already have uncertainty about crypto and NFT tax reporting, and it’s only increased as more people have engaged in the digital asset ecosystem (especially during tax season, as illustrated below).

Is DeFi affected at all?

In addition to digital asset exchanges and crypto-broker dealers, CARF places reporting requirements on any individual or entity that “makes available a trading platform.” Commentary in the CARF report elaborates upon this further, stating that an individual or entity makes available a trading platform if it exercises control or sufficient influence over the platform.

Several decentralized exchanges, such as Sushiswap and Uniswap, utilize governance tokens that allow tokenholders to put forth proposals that could influence the platform’s features. Consequently, CARF guidelines may burden token-holders with the same onerous and costly reporting requirements placed on large, centralized exchanges. This could lead to only large institutional players retaining governance tokens in these exchanges, eroding the democratic and decentralized value proposition these platforms offer consumers.

What happens next?

The OECD is working on creating an implementation package that ensures the consistent domestic and international application of CARF, which includes IT Solutions and other mechanisms that facilitate the automatic exchange of information. However, this process can take years, creating an opportunity for clarification on some rules that affect NFTs and DeFi applications.

Lastly, the implementation of CARF requires member countries to pass laws or create regulations following CARF guidelines. For example, the US chose not to adopt the CRS and instead moved forward with its own reporting regime under the Infrastructure Investment and Jobs Act in 2021. If portions of CARF remain unclear or unfavorably affect NFT issuers or DeFi participants, the US or other countries may choose to adopt their own tax reporting regime.