Summary

- A remittance is the process of transferring money as a payment or gift, usually on a global scale.

- Globally, about 1 in 10 receive remittances from family members working in other countries

- The remittance market is worth some $630 billion and on average, between $200 and $300 is sent home every month, with fees averaging out at 6% and wait times taking sometimes several days.

- A remittance using crypto is faster and more cost-effective – providing another option for family members sending remittances abroad.

- Read more CCI analysis pieces.

What is a remittance?

A remittance is the process of transferring money as a payment or gift, usually on a global scale. Remittances play a crucial role in sustaining families and bolstering the economies of developing nations. Approximately 800 million people receive money from family members abroad, suggesting that 1 in 10 people are involved in a market. The World Bank estimates the remittance market is worth $630 billion.

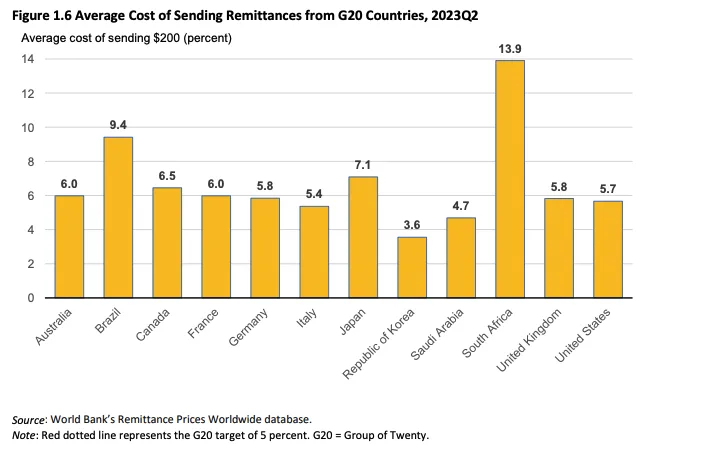

However, there are remittance challenges. The average monthly transfer ranges from $200 to $300. Reducing the fees associated with remittances is so important that the UN has made it one of its global goals. As of June 2023, it cost, on average, 6.20% to send $200, double the UN’s targeted rate for 2030. Sending remittances through banks proves even more costly, standing at 12.09%. While costs have decreased overall since 2009, cutting prices by at least 5 percentage points could save up to $16 billion annually.

Who sends remittances?

The US is responsible for more remittance payments than any other country. Some $81 billion flowed out of the US in 2022, a number that has doubled since 2002. Economies heavily dependent on remittances (as a percentage of their GDP) include Lebanon (54%), Tonga (44%), and Tajikistan (34%), while India tops the global charts for the amount received in remittances.

Remittance payments are increasing

According to the UN, “remittance flows to Africa doubled, reaching $100 billion in 2022, surpassing the funds received through Official Development Assistance and Foreign Direct Investment. In some African countries, remittances represent over 20 percent of Gross Domestic Product.”

Overall, remittance payments are expected to grow 3% every year, according to the World Bank. As numbers rise, there is growing concern about the accuracy and veracity of the data. This is crucial for two reasons: first, remittances represent a growing source of external finance for low- and middle-income countries, and second, the number of migrants is likely to increase due to “income gaps, demographic changes, and climate change”. Having clear and accurate data is necessary for policy-makers and governments, as well as international organizations to ensure sustainable development.

Crypto can reduce the time and cost of sending money abroad while increasing transparency

Crypto can help reduce the time and transfer fees associated with sending remittances. Ultimately, crypto allows for money to be sent across borders without the need for intermediaries, such as banks or other financial institutions, reducing the costs and times involved.

Crypto provides a degree of security when it comes to these cross-border transfers. The technology uses advanced cryptographic techniques to ensure the integrity and confidentiality of transactions. Due to its decentralized nature, there is no single point of failure in crypto that can be exploited. Blockchain technology ensures that all transactions are transparent because they are recorded on a public ledger, and essentially locked and sealed.

Even during periods of high congestion, crypto transactions take no more than a few hours to complete. For instance, sending Bitcoin to another wallet costs an average of $1.50 per transaction, and Ethereum costs an average of $0.75 per transaction for any amount.

Use of the technology is growing. For example, Bitso processed $3.3 billion in remittances from the US to Mexico, with a transaction fee of less than 1% – this is up from $2 billion the year before. BitPesa, operating in sub-Saharan Africa, combines traditional and cryptocurrency-based remittance payments with fees ranging from 1% to 3%. According to the UN, “Sending money to some African countries, such as Angola, Botswana and Namibia, can sometimes cost as high as 20 per cent of the amount transferred.”

As noted above, in many parts of the world, traditional banking services can be prohibitively expensive or simply inaccessible. Crypto transfers provide more financial inclusion and accessibility for people who do not have access to traditional banking services.

With crypto remittances all that is required is a computing device with internet access and a crypto wallet. Additionally, with a decentralized operating system, crypto transactions are not controlled by any central authority, which ensures that the transaction process is fair, transparent, timely and affordable.

Examples of crypto and remittance use

Several programs and platforms aim to address the challenges that traditional remittance payments processes pose. In December 2022, the UN Refugee Agency and the Stellar Development Foundation launched a pilot blockchain payment solution in Ukraine, providing financial aid through USDC to internally displaced persons.

MoneyGram’s announcement in 2023 of a non-custodial digital wallet, expected to be available in 2024, offers another glimpse into the evolving landscape of remittances. Although the wallet will be limited to the MoneyGram system, it will be subject to KYC requirements.

Remittances can be a lifeline for millions of families worldwide, but the high costs associated with traditional banking services underscore the need for innovative solutions. As we navigate the complexities of the remittance landscape, emerging technologies, blockchain solutions, and cryptocurrencies offer promising avenues for a more inclusive and cost-effective remittance economy.